Commercial Collections: An Overview

Commercial Collections

An Overview

By: Sherri Belanger, John Markham, Dwight Collings, Fabiana Fabbrini, Carmen Centeno, Brandy Sailers-Dow

Introduction: Balancing Act

- An action or activity that requires a delicate balance between different situations or requirements. (Google)

- An attempt to cope with several often conflicting factors or situations at the same time (Merriam Webster)

- Don't avoid extremes, and don't choose any one extreme. Remain available to both the polarities - that is the art, the secret of balancing. (Rajneesh)

- So be sure when you step, Step with care and great tact. And remember that life's A Great Balancing Act. And will you succeed? Yes! You will, indeed! (98 and ¾ percent guaranteed). (Dr. Seuss)

Conducting collections is a delicate balancing act. Credit professionals must steadily navigate through a whirlwind of choppy payment behavior and a fluctuating economic climate while nurturing positive customer relations and keeping their company’s business philosophy intact. In the end, their greatest strengths (their anchors in this storm) are the strategies they cultivate through trial and error. Quite literally – through experience. As a collector evolves, so should their framework of techniques.

From the very moment a credit application is obtained, the groundwork for the collection process begins. As in any significant relationship, periods of success and challenge are expected. The venture begins with cooperation, negotiation, and the excitement that each party will contribute to a shared goal of prosperity and satisfaction. The risks of entering the commitment, of course, are heavily weighed. Throughout the relationship, there are reminders about promises made and the importance of maintaining high standards. Add to this the emotional element of internal/external stressors on this professional bond, and the collection process becomes a sensitive component that can make or break a business relationship. A credit professional must develop their collection techniques if the alliance is not only to survive, but to thrive long-term. Again, a delicate balancing act.

The ultimate goal in collections is to maximize cash flow by facilitating sales and to minimize risk. To do this, credit professionals must continuously improve their collection performance, influence, and attitude. The collection-related strategies below are presented in the following collaborative piece:

- Credit Application

- Debtor Identification

- Negotiation

- Managing Emotions

- Timeline for Collection Activities

- Bad Debt Accounting & Collection

- Effectively working with Sales

- Dunning Explained

- Global Connection

Credit Application

The credit application is the central piece of documentation in a credit file as a whole and is an ongoing “contract”. Essentially it is an agreement between a creditor and a debtor and it defines the terms and conditions of selling to a customer on open credit. In this section we will discuss what makes up the credit application, how credit professionals utilize it for decisions and as a collection tool, and the high level aspects of utilizing a credit application for legal purposes.

Depending on the type of trading relationship between parties, the components and details of a credit application vary widely. Some of the standard components in most applications include applicant information, references, terms and conditions and personal guaranty. The applicant information verifies the business name or sole proprietor information, the names of the principals/owners, billing information, length of time in business, type of business, state of incorporation, and other information that can be useful in identifying the company requesting credit. References are usually a request for bank and supplier payment history and can be helpful in determining credit worthiness. Customer financials are a good way to dig deeper on a customer’s credit worthiness. In some instances, however, it may be impractical to obtain reliable financial information from the customer. In these cases, credit decisions must be based on more qualitative factors such as character, management competence, and market position.

The terms and conditions portion of the application explains the details of the credit relationship which, after signed, becomes an agreement between the creditor and the debtor. This includes the terms of sale (ie Net 30), any fees associated with past-due payments (interest or legal fees), whether the creditor has the right to enact a security agreement (blanket or PMSI), and what circumstances trigger default. Lastly, some applications may include a personal guaranty. This is a separate agreement which, when selling to a corporation or limited liability company, means that an individual (usually an officer of the company) will personally guarantee payment in the event of default.

Other essentials that are useful in making a good decision include validating the customer’s legal entity, reviewing the customer’s business model and strategy, reviewing any prior experience with the customer (or businesses with similar ownership) and, if possible, planning a customer visit. A customer visit can be a good start to building a solid relationship with larger customers and provide an opportunity for the credit professional to see firsthand both the risk and potential of a company. All of these components enable a credit professional to make a better, more informed decision.

High level Legal Aspects:

A complete credit application will specify the ‘where’, ‘how’, and ‘when’ a legal action can be taken. Essential documentation for a legal case may be obtained while performing regular monitoring of the accounts receivable and documenting collection efforts. Actively working the aging ensures that customers are notified on time when their payments are due, leading to earlier detection of payment issues.

One thing to keep in mind before using legal action to collect a debt is the cost associated with an attorney and court filing. In many cases, establishing a payment plan or promissory note with defined terms can be a much more cost effective solution. During the collection process, negotiating with the debtor and being open to different paths of resolution can be the key to recovering delinquent past due invoices without going to court.

A customer may declare bankruptcy if they cannot meet their obligations and in some cases, they may still be operating their business during the process. If a creditor is made aware, by any means (report/ certified letter or customer/legal advice), that a customer has filed for bankruptcy, the law protects the customer and all collection efforts on the past due debt must stop. This is called an automatic stay and trying to collect on the antecedent debt, even sending a statement of account, is prohibited by law unless there is an exception through the courts. Credit professionals should be aware of the state and local laws regarding commercial debt collection.

The credit and collections team hopes to avoid having a customer declare bankruptcy or having to write off bad debts. By taking the time to develop a robust credit application process and performing due diligence, credit professionals can realize the ultimate goal- minimizing risk to the organization while growing sales. Building a successful trade relationship requires a good foundation and strong framework, starting with the credit application and followed by effective account management. For a sample credit application, please go to:

http://web.nacm.org/resourcelibrary/CreditManual/creditapplicationandagreementexhibit.pdf

Mananging emotions in the world of collections

Whether a credit professional has worked in collections for a short time or for many years, the collector eventually comes to understand that the very nature of collection work oftentimes places them into situations where they must respond to upset, confrontational customers. Voices are raised, conversations get heated, and blood pressures rise. The customer, frustrated with their issue, sends a scathing email or calls at the height of their stressful moment to express their dissatisfaction for the company.

Fair? No. Understandable? Probably. Unresolvable? It depends. An opportunity to build a stronger relationship? Most definitely yes.

Collectors are often seen as people who pursue and pummel debtors to succumb to their will. As villainous as that may sound, it’s how they are generally perceived. A collector’s greatest power, however, lies not in the ability to provoke - It lies in the capacity to exert positive influence and in the talent for conflict resolution. If a credit professional enters a collection call with a negative attitude, they are only begging for a similar response. Yet, if they approached a customer with a positive, helpful attitude, it puts the client in a position where they see they will benefit from mutual cooperation. When it comes to resolving payment conflicts, attitude is key.

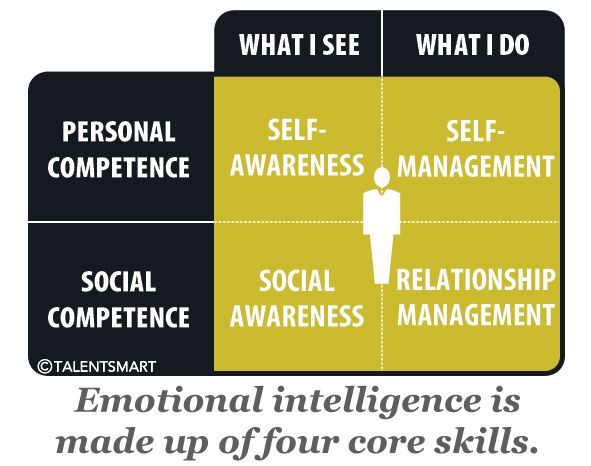

Emotional Intellegence

Ever heard someone say, “He has a high IQ, yet he lacks emotional intelligence?” What does it mean to have a high or low emotional intelligence (EQ)? Highly effective collectors usually display a high level of emotional intelligence whether they realize it or not.

Having a high IQ means that one’s logic, abstract reasoning, learning ability, and memory capacity are top-notch. However, a high IQ does not guarantee an individual is good at making judgments in real-life situations. (Shane Frederick, “Why a High IQ Doesn’t Mean You’re Smart,” som.yale.edu 11.01.09)

On the other hand, a high EQ can help a person analyze a difficult situation, determine the best course of action, and use it to their advantage, regardless of their IQ. Having both a high IQ and a high EQ makes one a power-user of influence. Without a good dose of EQ, however, the IQ can only go so far in social, work, and relationship scenarios. It behooves collectors to sharpen their EQ so they can be highly effective in their field, as they are at the precipice of customer-company relationships.

The good news is that although IQs are permanent, EQs can be improved upon with awareness and practice. EQ is comprised of four proficiencies:

(Travis Bradberry, “About Emotional Intelligence,” TalentSmart.com 2017)

The key to improving one’s EQ is to identify where one’s emotions come from, then analyze why and how one typically reacts. EQ steadily increases as one connects their inner self-awareness with their outer social-awareness. This is not to say that all emotions must be stifled. Rather, they should be used as a compass to navigate how one should react in certain situations.

For example, a credit professional may have to call a debtor whose name they are all too familiar with. Perhaps the customer is known for her argumentativeness and sharp tone on the phone. Anticipating the call, the collector is filled with reluctance and negativity. Emotions are apparent as the collector tries to control the conversation immediately, not letting the customer get a word in edgewise. He cuts her off as she tries to make a point so that the customer does not gain control of the discussion, trying to avoid an earful of negativity. The collector cuts the call short and tells the client he’ll email the details before quickly bidding her farewell.

The credit professional may have ended the conversation, but he did nothing to improve the situation. His feelings about her have not changed, and he has actually given her more reason to protest. And he is now farther away from a solid payment plan.

Using one’s emotional intelligence means (1) anticipating one’s own feelings and how one would normally react, (2) stepping back to assess if that reaction would be productive or prohibitive, and then (3) formulating a better way of solving the situation so that both customer and collector feel respected and satisfied. Sometimes it simply means making that important call after lunch when one has had time to nourish one’s body and regain energy. Sometimes it means opening the phone-call with a bright and cheery greeting. (Collectors don’t always have to be the voice of doom.) Perhaps it means being an active listener and letting the client vent as much as she wants before offering a calm and reasonable solution. Maybe it means talking to someone who is not emotionally invested in the issue and getting an outside perspective first. Sometimes it just means reminding one’s self to take a few deep breaths and not take things personally.

Go to the following link to take an EQ Test: http://www.ihhp.com/free-eq-quiz/

Let go of the ego

Collectors differ in personality and approach, however their persistence, drive, and ability to pursue payment under challenging circumstances are what make them successful at what they do. Doing otherwise would not only undermine their objectives, but would also ensure that their longevity as collectors would be short-term.

Credit professionals all strive in their own way to keep their companies thriving and afloat by ensuring timely payment for goods and services. It is pleasant to work with customers who are conscientious and who pay on time. Still, one’s true professional worth shines through when one is able to resolve payment conflicts in the face of blatant reluctance or lingering hardship. These types of encounters are not for the passive or the easily flustered. They require a high level of self-confidence and tenacity. Yet, these attributes, if not managed properly, can often add fuel to the fire. Aside from working within the laws developed in recent years to prohibit overzealous collection activity, it is important for collectors to be mindful of how their rapport with customers can either set the tone for calm resolution or ignite fiery resistance.

The ego is an important asset. It helps individuals accomplish their goals by giving them the courage to believe in themselves. A healthy ego propels one to go after what one wants with confidence. But too much ego (often accompanied by a thin skin) can often alienate customers. Ask anyone who works for the Sales Department of a company how important the relationship is between a company and its customers. One will hear tales of how the fussiest client was won over by a few simple accommodations and a soft touch. Or, how a long-time loyal customer closed their huge account because of how they felt they were spoken to by a single customer service representative.

Even when a credit professional knows they are right and the customer is not so right, arguing with an air of condescension only makes matters worse. It may feel natural (almost instinctive) to fight back and protect ones ego from customer attack, but no one ever wins in this scenario.

“There is a fine line between being egotistical and being confident... Ego says “I can do no wrong”, whereas confidence says “I can get this right.” Confidence says “I’m valuable” while ego says “I’m invaluable.”... As long as that confidence stays inside, you will follow that individual to the end. The moment that confidence comes out (and inevitably starts to grow with every assertion), other people lose faith and stop believing.” (Jayne Coles, “How Important is Ego in Your Career?” www.linkedin.com 10.14.15)

Collectors are often judged by the amount of money (and how fast) they collect. Timing is everything in the collections’ world. Amassing the most payments is one of the most gratifying parts of collection work. However, one mustn’t forget that the numbers are achieved only so long as relationships with clients are maintained and nurtured. This is an ongoing process that should never be taken for granted. As a collector, tone and word choice are vital to keep that relationship going.

In most cases, companies want their staff to accumulate the most funds possible, but not at the expense of losing future business prospects.

“Be sure to keep in mind what your words are actually saying to the consumer. Will the results be positive for everyone or will the consumer walk away with a negative feeling and result? You have the power to affect that choice.” (Bill Lindala “Stay Calm and Collect It,” p. 20. 2016)

Tone is definitely a skill to be practiced, whether it is in an email, letter, phone call, or face-to-face interaction. Tone should be professional, gracious, and should always display a willingness to help. Take, for example, the following questions:

- When can we expect payment?

- I’d like to help you resolve your balance. How can I assist you?

The first question, although valid, elicits defensiveness. The second question builds confidence and shows a readiness to help. Customers who feel a creditor is on their side are not only more willing to resolve balances, but also are more forthcoming with financial information that can help the creditor assess their current economic condition. This is knowledge which one can’t afford to dismiss, especially when it can help one assess and predict financial behavior. Not only does one gain payment info, one also gains valuable insight. Customers who are put off by a negative “us vs. them” tone aren’t as willing to provide such information.

Tone makes a huge difference in how people react to credit professionals. Harnessing one’s tone to gently influence customers to provide much-needed information not only benefits one’s companies, but also increases one’s ability to better direct customers in the long-run.

Collectors constantly compete with other vendors for the attention and consideration of debtors. Collection calls are fertile ground for emotionally-charged dialogue. The common tactic may be to command payment behavior with an assertiveness and alarm far above other creditors in the industry. Yet, a gentler, more mindful approach may actually induce cooperation from the customer that goes far beyond a single pay-out. A credit professional can make their case (and call) stand out by managing the discourse in a variety of ways:

- Using empathy - a key indicator of emotional intelligence

- Showing others that you understand their feelings

- Checking with them that you understand the problem

- Being clear about the endgame - solutions that satisfy both needs

- Gaining attention

- Collaborative language and problem-solving

- Providing the basis for positive future work

- (Dr. David Walton, “Emotional Intelligence - A Practical Guide,” p. 128. 2012)

Working with Sales

Working effectively with sales is very important to the overall success of the credit department. The challenge, however, is to keep the relationship positive since the sales and finance team can sometimes be viewed as having conflicting priorities and the dynamic can be complex. It is generally clearly understood that the sales department is concerned with generating business for the company, however credit professionals also have an important role to play in securing new business and protecting existing business. By working with new customers to determine the best payment terms available to them, the credit department is facilitating sales and fostering a relationship that is able to survive difficulties and hopefully thrive over time. Working with marginal accounts, especially those with difficult cash flow issues, allows the creditor to preserve existing business and may lead to a stronger relationship with the debtor once the issues are behind them, potentially leading to an increase in future sales. Although the dynamic between sales and credit can sometimes be seen as contentious or having conflicting priorities, the truth is that they share a common goal- strong sales. After all, it’s not a sale until the product is paid for. Sales is a valuable resource; they are the eyes on the ground, they are key to business intelligence, and they can be a sounding board in difficult situations. It is important to develop a positive working relationship with sales team.

The fact is that many credit departments are located in a company building and have little to no face to face interaction with customers. Unfortunately this puts the credit department at a disadvantage; a walk through a customer’s store may reveal shelves full of inventory, perhaps covered in dust, or a store that sees very few customers during the day. These may be warning signs of trouble and they are impossible for a creditor to observe without visiting the customer’s location. Sales can be a creditor’s ‘boots on the ground’ and can relay potential areas of concerns thereby helping the credit department to better understand the challenges that a customer is facing. Conversely, the sales team can also confirm increases in business, expansion of facilities, and opportunities for growth. By engaging with sales, a credit department is able to gain valuable insight into a customer’s operations, enabling them to make better decisions.

In addition to providing valuable quantitative information, the sales team generally has a closer relationship with the customer than the credit department and can provide insight into the customer relationship. This insight can prove useful when needing to convey a difficult message to the customer. If it becomes necessary to reduce payment terms or require prepayments going forward, sales should be made aware of the change and offered an opportunity to participate in conveying the message. The credit team should be careful not to depend too heavily on the sales team to deliver bad news, since the relationship between the customer and salesperson is a valuable asset. At a minimum, a sales person should be aware of changes in a customer’s terms or issues that could upset the relationship so that they are not caught unaware. These small considerations will help to ensure that the sales team and the credit team maintain a good working relationship.

Working with marginal accounts can be challenging for both sides of the sale but it can also provide unique opportunities for the sales and credit teams to partner together. Marginal accounts are usually considered to have less favorable references or financial information that would cause concern over extending open credit. Often sales is not aware of the existence or details of negative information and the credit team is tasked with balancing the desire to make a sale with the need to manage risk. Communicating concerns to the sales team, especially regarding financial information, should be done as tactfully and professionally as possible. Instead of declining the sale altogether, the credit team looks for a way to facilitate sales. Instead of framing the credit decision as ‘yes’ or ‘no’, the credit team may instead consider ‘how’. An account that may warrant prepayment today could very well warrant terms in the future and the credit department should take extra care in delivering a message that will keep the lines of communication and the road to increased future sales open.

Good communication and respect are the cornerstone of any good relationship and the sales-credit dynamic is no different. A good credit professional seeks to engage sales in good times and bad, knowing that the results will pay dividends for not only their individual departments, but the company as a whole.

Understanding the Debtor

Behind every debtor is a unique story waiting to be unraveled. It is a credit professional’s responsibility to read each debtor prudently so suitable credit decisions can be made. The first question to be answered is why the customer has fallen behind in their payments. There are many reasons why a customer could be in arrears and each scenario may need to be handled differently. In instances where delinquency is an unusual event for the debtor, and they are forthcoming with reasonable information and can provide a solid plan for future payment, it may be possible to come to a quick and easy agreement. However, it is the debtors who choose to withhold critical information, promote falsehoods, or are, perhaps, naïve to the state of their business health, who creditors must approach cautiously and probingly. Signs that credit professionals must look for in order to prevent loss and prepare for any negative impact on the company are:

| Loss of income | Over-commitment | Debts left by former partners |

| Natural disaster | Theft/fraud | Disruptions in the industry |

| Working the system | Withholding payment | Disorganized AP |

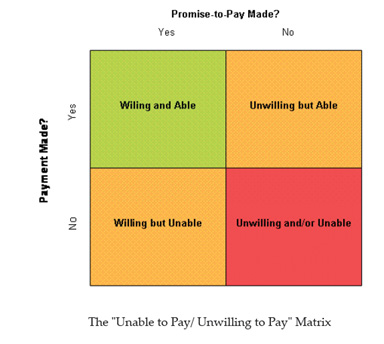

Although collectors must treat all types of debtors professionally and respectfully, the strategy and approach can differ for each scenario. Before determining what course of action to take, a collector must find out which category the debtor currently falls. Does the debtor show a willingness to pay down the debt, but is unable to do so for the next several weeks due to cleaning up after a major storm? Is the debtor more than able to pay, but is unwilling due to delayed issuance of credits for returned product on the creditor’s part? Does the debtor show no signs of being able or willing to pay – possibly, missing in action? Once a credit professional determines the debtor’s status, it is easier to come up with an enforcement plan.

The green shaded area in the illustration below signifies there are no obvious reasons for alarm. Business as usual. The orange shaded areas do indicate a cause for alarm; however, there remains optimism that issues can be resolved with continued communication and a little nurturing offered from both sides. The red shaded area is a signal that it may be time for the creditor to cut their losses and to initiate the referral process.

(Brendan Le Grange “Collections Strategies – The Unable to Pay / Unwilling to Pay Matrix,” https://blegrange.wordpress.com 3.24.09)

It is important to note the fine line between offering flexibility in good faith and allowing one’s self to be taken advantage of. It is important to gather as much information about your customer as possible to determine the risks of seeing the business relationship through difficult times. It is often useful to reach out to one’s sales people in the field as well, as they can be a credit professional’s best eyes and ears. Once information is provided, and the financial condition and payment attitude has been assessed, a creditor should implement the following strategies:

| Willing and able? | Continue to nurture a close, mutually beneficial relationship. |

| Willing but unable? | Establish debtor’s payment limitations. Listen closely. Is delinquency a temporary instance or downward trend? Payment plan can be offered if sensible to do so. Important to uphold relationship while customer resolves. Flexibility should be shown, but not in excess. |

| Not willing but able? | It is critical to act immediately and to use leverage appropriately. |

| Not willing and unable? | All options exhausted. Expedite referral to in house special collections or outside collection agency for further handling. |

“Knowing when to work with the debtor and when to draw a line in the sand is paramount. Asking probative questions and listening for the answer will assist in determining ability and willingness.” (http://EzineArticles.com/expert/Patrick_H_Hale/430046)

Some customers try to keep collectors in the dark regarding their financial distress. It is important to be aware of any warning signs before matters become too big to control. Credit professionals can locate signs of insolvency and non-liquidity in a customer long before the at-risk behavior begins to have a detrimental effect on the creditor. This information can be found in business newspapers, trade association reports, and other publicly available documentation. However, it is very important to know the authenticity of your sources before coming to any conclusions.

Some warning signs that serve as red flags to the credit professional:

- The debtor has stopped discounting bills

- There is a general slowdown in payments to vendors

- Lawsuits are being instituted against the debtor

- Tax liens or vendor liens are being filed against the debtor

- The debtor is constantly shifting from one source of supply to another

- The debtor is in default with its lending institution(s)

- The financial condition of the company is deteriorating

(NACM, “Principles of Business Credit,” p.424, 2013.)

Timeline for Collection Activities

Every company should have a comprehensive credit and collections policy which includes guidelines related to aging receivables. Management and the Credit departments generally have targets related to Days Sales Outstanding (DSO), aging tolerances, and bad debt which should be considered when creating a timeline for an organization’s collection activities. The National Association of Credit Management (NACM) provides a wealth of information for organizations that are seeking to create or update policies that reflect best practices in credit and collections.

Following a comprehensive credit policy, collection success begins with good information. Invoices must contain accurate data regarding the customer’s account and charges to the debtor; missing or incorrect information will greatly hinder even the best collector’s efforts. Invoice disputes should be corrected as quickly as possible and it is advisable to consider a policy which requires invoice discrepancies to be communicated to the organization within a certain number of days. Resolving invoice disputes becomes increasingly more difficult as an invoice ages. Accurate contact information is also critical to the successful collection of invoices. It can be disappointing to direct one’s efforts to an incorrect contact who does not respond, delaying collection time and wasting resources.

While some companies choose to begin collections before invoices are due, others choose to collect when the account is past due. Sending regular statements can help a debtor stay on top of their payables and may reduce manual work down the road. While the details of a collection policy may differ between organizations, the timeline for collections generally begins gently and escalates based on the risk to the receivable.

Initial contacts with a debtor should contain a friendly request for payment. There are a number of reasons that payment may have been legitimately delayed- an unresolved invoice dispute, a keying error in the payables system, a business event, a life event (in smaller companies), a quality issue with the invoiced item, or even a misunderstanding. It may be beneficial to include in the friendly reminder an offer of assistance, such as “If there is anything that may be preventing the invoice from being paid, please let us know immediately so that we may be of assistance.” When an initial contact for payment is not successful, it is important that collection efforts be consistent and increasing in urgency. Early requests for payment may also consider the payment history of the debtor; if payments are chronically late and there is little communication to indicate that delays are due to isolated issues, it may be advisable to influence payment behavior using a tighter collection timeline or leveraging resources.

Timely collections is essential to managing a healthy receivables portfolio. The value of a receivable declines over time because the likelihood of collection decreases the longer that a receivable is outstanding. An aging schedule predicts the collectability of receivables based on their aging bucket, expressed as a percent, and assigns a value to the receivable. For example, if a customer owes $10,000 for an invoice that just came due, that receivable is valued internally at 100% because the likelihood of collection is high. As the receivable ages and the likelihood of collection is reduced, the value of the receivable is also reduced. If a company has valued receivables over 90 days at 50%, that invoice is now worth $5,000. That is not to say that the debtor only owes $5,000 because the debtor still owes the entire $10,000- rather, that is the internal value that the creditor has placed on the receivable as an asset. Not only does the likelihood of collection decline over time, but the resources that a collector has used in trying to collect the debt represent a cost to the organization.

If initial contacts have proved unsuccessful in securing payment and it has been determined that the payment delay is due to either an unwillingness or an inability to pay, the creditor should increase the frequency and tone of the contacts to reflect the urgency of their request. Some companies use dunning letters or a dunning strategy that mirrors their collection policy. The schedule that a company uses is unique to their business and considers their market, capacity to leverage, level of risk, and the overall relationship with their customers. A greater explanation of the dunning process is explained in the next section.

Generally after a certain number of unsuccessful attempts to collect, the creditor will send out a final demand. A final demand is the last step before collections and may be a precursor to, or a substitute for, a third party agency’s 10 day letter. It is important to know what the third party collection agency offers in terms of support services, how much the third party agency charges for collections, and what type of tone the agency takes in collecting on your behalf. They become the face of the creditor they are representing and therefore should present themselves in a manner the creditor would approve of.

Once an account has been referred to a third party agency, a creditor’s credit and collection policy dictate whether it is going to be reserved for bad debt. Reserving for a receivable is not the actual action of writing it off, but it recognizes it is a receivable at risk of being written off. Some companies choose to write off bad debt once a receivable hits a certain age or once a third party collection agency has deemed it to be uncollectable. Accounting for bad debt is explained in a later section.

Dunning Explained

Dunning is not a word that is often heard outside of credit and collections but it is a process that we do often, even if we don’t know it. The word ‘dunning’ can be either a transitive verb (dunning a customer, the dunning process) or a noun (the dunning letter itself). ‘Dun’, according to Merriam-Webster, is a word from circa 1626 that means “to make persistent demands upon for payment.”

Dunning letters are, very simply stated, a standardized letter used to communicate with a customer regarding an overdue account that typically escalates in either frequency or tone until the balance is resolved. A company’s dunning process is the schedule which dictates when letters are sent out as the account balance ages. Dunning letters generally should contain the balance details, including the total amount due and the invoice detail, as well as a request for payment and contact details in case there are any questions.

Dunning letters and the process for sending them to overdue accounts is decided by the organization that sends them, according to an escalation schedule that the Accounts Receivable or Credit Department feels is appropriate. There is no set or ‘right’ schedule for dunning a customer; however it is important the entire collection process comply with all applicable laws. It is advisable that every credit and collections professional be knowledgeable about the laws that apply to their collection efforts.

Many ERP systems offer the ability to automatically send out dunning letters based upon customizable parameters that are set up in the system. This reduces the amount of manual work that an Accounts Receivable Specialist has to do to send out letters; however there is the risk that a customer may receive a dunning letter for an invoice that is a known issue or is being disputed. For this reason, it is important to be aware of the customizable features and built in logic for automated dunning processes.

A manual dunning process involves making requests for payment at regular intervals using phone, email, or regular post. Dunning language traditionally begins with a reminder for payment either before the invoice is due, on the due date, or shortly after the due date. A common school of thought is that payment reminders that are timed shortly before the due date prompt more on-time payments. Some companies prefer to wait until the invoice is due or until a grace period has expired before sending the first request for payment. This is a strategy that should be thoughtfully considered and discussed, followed by consistent implementation.

Initially, dunning letters should be a friendly reminder of a past due balance. If early dunning attempts are unsuccessful, there is usually an escalation in frequency and/or tone as collection efforts progress. It is important not to threaten or harass debtors in a way that could create a liability or damage a company’s reputation as a creditor, regardless of the action (or lack thereof) of a debtor. Maintaining professionalism throughout the collection process facilitates constructive discussion and is reflective of the integrity of the creditor.

Failure on the part of the debtor to respond to dunning attempts signals trouble for the creditor. If the contact information is correct and there is proof that the debtor has received the dunning notices without responding, additional intervention is needed. An organization’s credit and collection policy should contain a roadmap for escalating collection activities, potentially with a referral to a third party collection agency. It is important to keep accurate records of all collection efforts.

Negotiation

Every credit professional will engage in some form of negotiation in the course of their duties whether it be with customers, sales people, finance team members, or management. Negotiation is much like credit, both a science and an art, and reaching an agreement that satisfies the parties involved takes skill and talent. While many people engage in negotiations in their daily lives, for example buying and selling cars or property, credit professionals are constantly called upon to reach agreements that meet the needs of multiple parties and must do so in a way that will promote growth.

Successful negotiations start with a couple of key techniques. It is important to understand that one’s mood, tone, physical and mental position, and preparedness will have a direct impact on the outcome. Being fully prepared is not strictly limited to facts; rather it is the sum of many parts which include projecting the appropriate attitude and presence that will make others want to reach an agreement. Hunger, fatigue, distraction, discomfort, and nerves can all play a role in derailing even the best laid plan. Making sure the environment is conducive to success is a good first step.

Alternative plans are another key aspect of reaching an agreement. Usually a negotiation involves two or more parties whose agendas do not fully align and compromise or persuasion is necessary for a successful outcome. Each party has their own version of the best possible outcome but as a negotiation progresses and the individual parties adjust their definition of success, the well prepared negotiator has alternative outcomes in mind that also meet their needs. They are prepared with not only the best possible outcome, but they have identified the worst case scenario and have alternate proposals to suggest.

It is important to remember that a negotiation is not simply about imposing one's own agenda on others. Listening to the other parties is critical to understanding their position and by validating their concerns, a good negotiator is able to overcome resistance and gain support for a positive outcome. Anticipating objections and having answers prepared in advance can help to remove roadblocks in the process and will demonstrate that the credit professional understands the issues.

During negotiations there may be times of quiet or a lack of activity, as parties consider new information or are asked to revise their position. This quiet can be a tool that prompts the other party to offer a solution or to offer more information than they would have otherwise, had they not felt compelled to fill the silence. Embracing the silence not only projects confidence, it can result in the other parties making a move they were not fully prepared for. Incremental victories such as these may add up to overall success as long as the negotiator acts intentionally and with thought to the overall process. Remember too that agreements can sometimes take time to solidify. If discussions break down, knowing when to take a break and regroup may make a significant difference in the outcome.

For credit professionals, the most frequent area of negotiation involves customers who are unable to make scheduled payments. The customer may be asking for a payment extension or they may be asking for a payment plan, to space out payments on a large balance. It is important to first understand what is driving these types of requests; is this isolated incident or is the situation expected to continue short to long term? Has the customer made similar requests in the past and does this demonstrate a pattern of cash flow issues? Are there issues in the market that are impacting the customer's ability to pay? Are the reasons for the delay caused by factors under or outside of the customer's control? These are key questions the credit professional will need answered in order to make a decision.

Another area that can require negotiation is in regards to payment terms. A credit professional may do a credit review and grant terms that the customer or the salesperson feels is too restrictive. It may be reasonable to reconsider if additional information is made available, such as financial statements or references that were not considered in the original review. The credit professional may need to explain their decision and should therefore be prepared for such a discussion, especially since sales and credit must present a united front. Requests to change trading terms does not only happen with new accounts; established customers may also request a review of their account. Changes to terms should be met with a healthy dose of skepticism but also with an understanding of what is driving the request, asking similar questions as requests for payment extensions. If the customer is dealing with a temporary setback, it may be appropriate to help them work out a payment plan or other solution that will allow trading to resume under normal conditions in the near future. A request for a permanent change in terms will usually require additional analysis including the increase in the overall balance and risk, the impact to DSO, and compliance with the credit policy as well as anti-trust laws. A change in terms is unlikely to resolve serious financial issues and the credit professional should use caution when negotiating with customers in these situations. It is possible to help financially distressed companies through times of trouble, but having open communication and good follow up is essential.

Depending on the level of involvement with managing customer financial accounts, credit professionals may also be involved in resolving disputes related to pricing, shipping, or charge backs. Disputes can impact timely payment and in order to effectively resolve the issue, it is important to understand all of the facts before proposing a solution. Pricing issues can cause invoices to be held for payment and often times it may require assistance from an internal sales person or the customer's purchasing agent. There may have been special pricing that wasn't communicated at the time of order entry or there may have been a recent price change that has not been updated on the customer's side. The original purchase order is generally the best place to start, since it may have annotations or other purchasing information that will help resolution. If the solution is not simple or if the misunderstanding is not easily cleared up, it may be necessary to involve additional stakeholders in order to reach a solution. Before responding to a pricing issue, it is important to have as much information as possible.

Short shipments or incorrectly shipped orders will usually require a proof of delivery (POD), a packing slip, or a bill of lading. While these types of issues are common, resolution is not always easy. Comparing a packing slip to the customer's receiving log may be enough to resolve the issue but sometimes there are more complex factors involved. Requesting the debtor pay the invoice until the dispute is resolved is one option or the creditor may request payment for the items not in dispute while the issue is investigated further. Splitting the disputed amount or crediting back disputed items are additional possibilities, depending on the circumstances. It is up to the credit professional to be aware of the facts surrounding disputes in order to navigate to an equitable solution, understanding that sometimes compromise is the best way to preserve a valuable relationship.

The best advice for good negotiations and successful dispute resolution is to be to prepared, know the facts, and construct outcomes which, to the extent possible, are positive for all involved. Keep in mind:

- Before beginning any negotiation, make sure you are in a good state of mind. Having a calm disposition and expecting a positive resolution will help you to effectively engage the customer.

- Gather as many of the facts as possible and engage stakeholders as necessary. Reaching an amicable solution that addresses the real issue requires attention to detail and being open to outside perspectives.

- Have multiple possible outcomes available whenever possible and anticipate potential objections.

- Never give up. A credit professional who quits in the face of adversity will lose the battle. It may not be the right time to reach an agreement, but another opportunity might present itself that will allow for a successful resolution.

Bad Debt & Accounting

Bad Debt is defined by Merriam-Webster’s Dictionary as a, “loan that will not be repaid.”For such a simple definition, companies have found many different ways to interpret and account for their own bad debt. In some businesses, the bad debt is accounted for once an account hits a certain aging bucket (90, 120, 150 days past due), and in others an account won’t be written off to bad debt unless the customer is unresponsive or the debt has been discharged in a bankruptcy. The industry of a company, whether the company is publicly held or privately held, and the philosophy of management on bad debt will all dictate how and when bad debt is classified.

From a functional side, the accounting for bad debt can vary greatly from company to company. One way it can be accounted for is through monthly accrual on financials then at year-end the amounts get “trued up’” to mirror the actual bad debt being recorded. Another process used by companies is to write-off actual bad debt identified on a monthly basis. There are other variations on how to accrue and account for the bad debt on a monthly, quarterly, and annual basis.

In 2002 the Sarbanes-Oxley Act was passed, which refocused the need to truly identify bad debt correctly in publicly held companies and to create internal controls to ensure it was not understated in financial statements. Truly to follow the standard set forth by Sarbanes-Oxley, a company must show a consistent process for identifying and treating bad debt expenses which mirrors what they believe to be uncollectable. As a result many publicly held companies have become more conservative in how they account for bad debt expense.

The goal of any credit professional is to minimize bad debt expense. The problem with a complete focus on minimizing bad debt expense is it leads to a risk aversion mentality which will limit the opportunity to sell on a credit basis. The goal should be to balance risk to maximize profitability through sound credit management. Many companies today are driven on sales growth, which in many cases means finding the correct balance between risk of loss or bad debt, and the return from taking on a “risky” customer. Some businesses even have “risk- based pricing” to account for the varying levels of risk to take on a customer.

Bad Debt Collection (Recovery)

Given that bad debt is defined as a “loan that will not be repaid,” it might seem like a contradiction in terms to discuss the collection of bad debt. Really, this speaks to the relentless nature of credit managers in the pursuit of collecting what has already been deemed uncollectable. The means and approach for collection does not necessarily change once an account is written off to bad debt expense, but if collected it will have a 100% profit hit as a reversal of the previous bad debt entry.

Even before a customer becomes a bad debt, there are many items that may signal that an account is struggling to repay a debt. The customer may not be returning calls, has a voicemail that is full, or in conversations states a struggle related to cash flow. Some of the adverse actions in the early stages by a credit manager could be a dunning letter, turning over to a collection agency, having an attorney file suit, or if a customer has filed bankruptcy filing your proof of claim or right of reclamation claim. When an account is struggling sometimes the best solution is coming up with a promissory note for a longer term paydown, or getting further security against another asset like a piece of property.

Once these avenues have been pursued without any results and the customer is still in business, a legal course of action can make sense if it is deemed cost effective. Filing suit to gain a judgment gives the creditor the ability to file a lien against property owned by the debtor or garnish a bank account. Even if these do not equate to payment in the near term, the judgment remains valid for a number of years (varying by state). The lien against a property can become valuable even years down the line if at that point the debtor wants to sell the property.

International Collections

As companies expand into the international marketplace, it can be easy to underestimate the challenges that come with selling beyond a company’s own borders and into unknown territories. While some challenges may be obvious, such as importation or foreign exchange rates, some challenges may be related to something more subtle- the ambiguous matter of culture. Globalization of business has outpaced the ability of many organizations to manage the accompanying cultural shifts. The focus of international credit and collections is usually concentrated on overcoming legal, political, technological, and economic barriers, while cultural barriers are often unacknowledged or discounted. The cultural diversity found in today’s global economy requires that those engaged in international credit and collection efforts be aware of the global influences on a business relationship.

Before examining the different nuances of global business, it is important to remember a couple of key points. First, the political and legal climate in both the country of the creditor and the country of the debtor will have a direct impact on trade. It is imperative that international trade obey the laws of the countries involved, especially laws regulating importation and taxation. Second, accurate information throughout the order to cash process is critical to the successful import, export, and payment of goods. It should not be assumed that the technological standard of one nation is the same as another. Having clear and comprehensive order to cash processes can alleviate and help to avoid some of the issues surrounding international trade. Before expanding into international markets, a creditor should make sure that invoicing is accurate, containing the correct legal billing name, billing address, payment terms, Value Added Tax (VAT) information (if applicable), shipping address, invoice date, due date, article codes, prices, discounts, and origin information (if required). Correcting errors on international invoices can cause delivery and importation delays or in extreme cases, issues at customs that could impact future trade. It may also be advisable to email invoices; especially those that have far to travel via post or that may be destined for an area with weak infrastructure. Creditors should familiarize themselves with all of the legal requirements for dealing with countries into which they would like to expand. Finally, having someone who can provide language support for international customers is an invaluable tool for a creditor. Collecting or negotiating in one’s own language can be daunting enough without the added stressor of poor communication.

Although these suggestions are intended to help build a strong foundation upon which to expand or enhance trade with other countries, it is important to remember that all communication must be based in mutual respect and consideration. Cultural missteps can be forgiven and overlooked when parties work together but failing to value or appreciate a customer transcends questions of culture or custom.

EMEA - (Europe, Middle East, Africa)

The EMEA Region is a very short acronym for a very large area of the world that includes Europe, the Middle East, and Africa. Due to the vast cultural and even subcultural differences of these regions, it would be unwise to make broad generalizations in regards to cultural influence or business practice. Instead it is advisable to seek out resources and agents within the respective countries that specialize in trade and collections regulations. Lawyers in-country are not only qualified to represent creditors in court, they are also valuable resources for drawing up contracts and advising on business decisions before litigation becomes an issue. Legal counsel can be expensive however, and resources such as the Finance, Credit, & International Business Association (FCIB), Export.Gov, and local sales associates can be helpful sources of information.

South of Europe - Mediterranean countries

Many of the businesses in Mediterranean countries are family run and multi-generational. For this reason it is advisable to exercise care in maintaining the relationship to preserve trade. It is not uncommon to spend time socializing and exchanging personal information over a meal whilst discussing business. These types of customers may prefer a more personal style of account management, especially when dealing with difficult situations such as negotiating payment plans. In Italy, Spain, and Portugal, although the EU Directive on payments and terms is very clear and standards are required under the Directive and EU law, many of the companies in these areas have traditionally expected longer terms. Managing these expectations can be difficult and the desire to retain longer terms remains. It is important to note that the EU Directive only applies to trade between EU countries; therefore a US exporter selling to a country in the EU would not be bound by the Directive. At the time of this writing Greece continues to be under capital control, meaning that payments issued to foreign companies need to go through an approval process at the bank; this process can be long and bureaucratic.

Eastern Europe (Bulgaria, Czech Republic, Croatia, Hungary, Romania, Poland, Slovak Republic)

In Eastern European countries, customers are accustomed to working on a prepayment basis or being insured by third party companies for extended credit. Amicable and confidential approaches to resolving disputes are usually looked upon most favorably, especially if it is possible to conduct business in person. A professional demeanor combined with a personal element, such as a site visit, typically adds value to the management of these accounts. Business culture generally resists the payment of interest fees for late payments, despite the EU Directive which defines not only the maximum rate for interest but also the minimum fee for a late payment (presently €40). It is again important to note that the EU Directive applies only to trade between countries in the European Union. For US companies selling into Eastern Europe, the EU Directive does not apply.

Central Europe

Central Europe is comprised of some of the world’s most highly developed economies. As such, it might be easy to assume that credit comes with lower risk and that invoices will be paid timely, however creditors should still exercise caution and perform due diligence throughout the order to cash process. According to a report published by Market Invoice entitled “The State of Late Payment 2016”, the countries of Central Europe pay at or before the due date on approximately 40% of invoices. According to Businessculture.org, businesses in this region generally appreciate punctuality, conservatism, and adherence to agreements. Belgium is known for being slightly less formal and generally conflict averse.

Scandinavia

The Nordic countries of Northern Europe generally have a high standard of living, value egalitarianism, and expect punctuality, according to Businessculture.org. Denmark and Sweden trade heavily with Germany and the Netherlands, all countries which belong to the European Union (Europa.eu). Notably, Norway and Iceland are not a member of the EU and because of this, trading with EU countries requires additional customs documentation. Norway is, however, presently a member of the European Economic Area and part of the European Free Trade Association. According to the Market Invoice report, “The State of Late Payment 2016”, companies in this region generally pay close to terms.

UK & Ireland

With the vote on the Brexit and the exit from the EU in 2019, new challenges will arise due to changes in the trading regulations with the UK, including new customs laws and taxes. One important consideration for the UK and Ireland is that the trading currencies are different for each- the UK trades in GBP and Ireland trades in EUR. Another notable difference is that, according to Market Invoice’s “The State of Late Payment 2016” report, Ireland generally pays on time while the UK averages approximately 6 days late. The UK is still very traditional and prefers to do business in person; spending time winning over a customer may pay dividends later on. A beer and light conversation about football (American soccer) can create an opportunity for a more informal business discussion, though it should be noted that people can be very passionate about the teams they support.

Russia

In Russia and most of the CIS countries (Commonwealth of Independent States), business discussions are frequently done at lunch or dinner where socializing and entertaining has a large impact on dealings between companies. Due to the sometimes informal nature of this approach, it is very important to have contracts that contain clear and concise details including payment terms, credit limits, bank information, and product access. Agreed changes to contracts should be formally amended or entirely rewritten to avoid any misunderstanding. Default in payment could result in damage to the debtor’s business reputation; for this reason, customers experiencing issues will often suggest a payment plan to the collector and abide by it. Companies in these areas are accustomed to having to prepay for orders due in large part to the difficulty in finding trade or financial information. When customers are eligible for open terms, they may still pay in advance- especially if there is a favorable exchange rate. It should be noted that Belarus presently has some currency controls in place that limit prepayments. Companies will frequently use one name for import trading (English) and another for doing business within their country (Cyrillic). Customs can be very bureaucratic and it can take a long time to clear shipments if there are discrepancies in the documents.

Middle East

Countries in the Middle East such as the UAE, Kuwait, and Saudi Arabia are used to working with Letters of Credits (LC’s), typically documentary LC’s. Standby LC’s are generally not used and documentary LC’s typically forbid interest charges. Documentary LC’s are paid according to the terms defined in the LC.

Standby LC’s are generally workable in Turkey; however the fluctuation of the local currency can have a large impact on payments. There have been occasions when the exchange rate has been very low for extended amounts of time and the customer may wait until the last minute to purchase currency, usually USD or EUR. The Turkish business culture is generally very traditional and formal, preferring scheduled meetings and favoring punctuality, according to Businessculture.org.

India

The majority of trade is done using documentary LC’s, which can be time-consuming and sometimes confusing. Collections on accounts with open terms can be difficult, and delays are not unusual. Payment promises may not materialize and legal issues are based on common law. Active involvement in amicable debt collection, following proven principles of negotiations, and conforming to local terms are key features to successfully collecting in India. By keeping in close contact with the debtor, credit professionals are able to distinguish between genuine cash flow problems versus stalling tactics and non-payment. Field visits and face-to-face meetings with the debtors can be very helpful in the collection process.

South Africa

South African Law has Roman Dutch origins and the debt collection process is well entrenched within the system. However, due to the fact that South Africa remains a developing country, corruption and fraud remain rife and a weak currency greatly affects the debtor’s ability and/or willingness to pay. Delivery time and customs are also some aspects a collection professional should consider.

North Africa (aka Maghreb: Tunisia, Algeria, Morocco, Libya)

Debt collection can be difficult in Maghreb countries. Many debtors try to avoid payment with a range of delaying tactics, which collection professionals have to deal with. The legal system can be inefficient, much to the detriment of creditors. Due to the events of the Arab Spring in 2011, collection opportunities have become even more difficult. In Tunisia, political unrest has led to destruction, vandalism and the burning of assets and commercial premises, which has forced many companies out of business. When trading with Tunisian or Algerian companies, it is highly recommended to obtain bills of exchange covering the whole debt prior to delivering the goods thus avoiding future discussions and allowing creditors to file a Payment Order in case of non-payment. Algeria has tried to limit imports and has restricted trading terms to LC’s or CAD. Documentary LC’s that are controlled by the bank are held to very strict standards and even small discrepancies will cause payment to be withheld. Customs regulations are also very strict and combined with the bank’s restrictions, it can be very difficult to trade in this country.

Mexico

As with many Latin American countries, business dealings rely heavily on interpersonal relationships. The attention paid to developing relationships and making contacts could easily be viewed as an investment in the success of the business partnership. Pagarés, literally translated as “will pay”, are promissory notes which include very specific language and, if properly executed, may help facilitate trade. Court systems in Mexico shares more in common with other Latin American countries and Europe than it does with the US, relying heavily on civil law which is a mix of Ancient Roman, Canonic, and Medieval Merchant law. Due to the complexity and differences between US and Mexican legal systems, it is advisable to consult a lawyer experienced with Mexican law when pursuing a legal course of action.

South & Central America

Like Mexico, South and Central America rely heavily on interpersonal relationships. Countries in this area vary in regards to the general level of formality; however respect for the individual and increasing incrementally to senior leadership is especially important. Collections in SCA can become more complicated in countries where Customs and the Central Bank are heavily involved in trade. It is critical that collection efforts in these countries be done with an understanding of the trading environment including the political, financial, and interpersonal factors that influence the creditor/debtor relationship.

Asia

According to WorldFinance.com, China does not officially allow ‘collections’ due to a law from the 19th century that allows only legal entities such as the police or court system to collect debt. Despite this, many companies do provide debt collection services by billing their services as risk management or credit consulting. Since honor is an integral part of Asian culture, payments are generally received timely and insolvency is frowned upon (Worldfinance.com). Payments in Indonesia are the most likely to encounter delays. Common payment methods are bank transfers and drafts.

Oceania

Differences in the time zone should be acknowledged and planned for, especially in regards to communication and making ship/hold decisions. Payments are mostly issued by bank transfer and, according to the Market Invoice report “The State of Late Payment 2016”, payments averaged 26.4 days late. Generally speaking, collection efforts can mirror those that someone would use in the US but it would be good practice for the collector to be acquainted with the challenges of exporting into this area. Sea freight is preferred by many customers since air shipments can be very expensive, however it can add a considerable amount of time onto delivery of the product.